Capital Intensity, Scientific Breakthrough, and Complex Coordination

Excerpts from Peter Thiel's 2014 Stanford lecture, "Competition is for Losers"

In 2014, Peter Thiel gave a famous lecture at Stanford titled, “Competition is for Losers.” You can watch the lecture here, and there’s a transcript available here. I highly recommend watching it end to end, but for those without that time I pulled out my top 5 nuggets of wisdom relevant to building the durable, venture scale companies we aim to back at Also Capital.

On the Durability of Scientific Breakthroughs: “There's always this question about having a huge breakthrough in technology, but then also being able to explain why yours will be the last breakthrough or at least the last breakthrough for a long time or if you make a breakthrough, then you can keep improving on it at quick enough pace that no one can ever catch up. So if you have a structure of the future where there's a lot of innovation and other people will come up with new things and the thing you're working on, that's great for society. It's actually not that good for your business typically.”

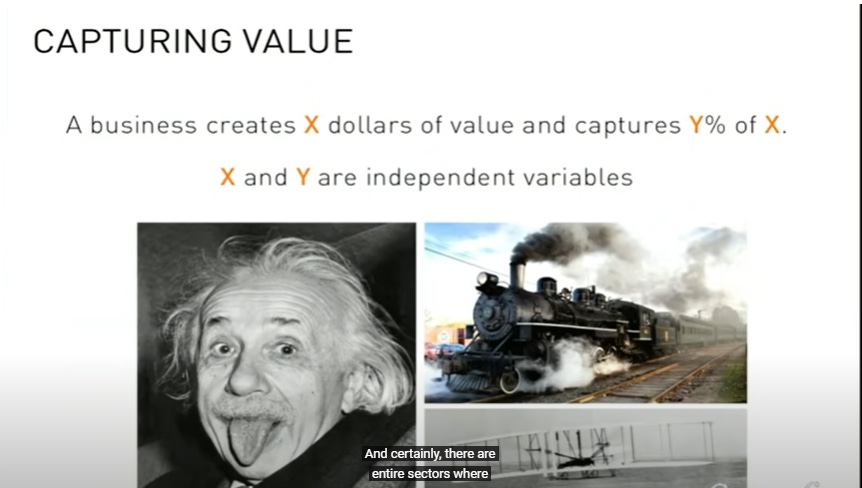

On Capturing the Value of Scientific Breakthrough: “…some of these [technological innovations] can be extremely valuable, but the people who invent them, who come up with them, do not get rewarded for this…Even in technology there are sort of many different areas of technology where there were great innovations that created tremendous value for society, but people did not actually capture much of the value. So I think there is a whole history of science and technology that can be told from the perspective of how much value was actually captured.”

On Monopoly via Complex Coordination: There are, in my mind, probably only two broad categories in the entire history of the last two hundred and fifty years where people actually came up with new things and made money doing so. One is these sort of vertically integrated complex monopolies which people did build in the second industrial revolution at the end of the nineteenth and start of the twentieth century. This is like Ford, it was the vertically integrated oil companies like Standard Oil, and what these vertically integrated monopolies typically required was a very complex coordination, you've got a lot of pieces to fit together in just the right way, and when you assemble that you had a tremendous advantage. This is actually done surprisingly little today and so I think this is sort of a business form that when people can pull it off, is very valuable. It's typically fairly capital intensive, we live in a culture where it's very hard to get people to buy into anything that's super complicated and takes very long to build. When I think of my colleague and friend Elon from PayPal success with Tesla and SpaceX, I think the key to these companies was the complex vertically integrated monopoly structure they had.

On the Importance of Market Structure to Investment Returns: “I do think the history of innovation has been this history where the microeconomics, the structure of these industries has mattered a tremendous amount and there is sort of this story where some people made vast fortunes because they worked in industries with the right structure and other people made nothing at all because they were in these very competitive things.”

On Value Capture in Science vs. Technology: “The railroads were incredibly valuable, they mostly just went bankrupt because there was too much competition. Wright brothers, you fly the first plane, you don't make any money. So I think there is a structure to these industries that’s very important. I think the thing that's actually rare are the success cases. So if you really think about the history in this and this two hundred fifty years sweep, why it’s almost always zero percent, it's always zero in science, it's almost always in technology.”